Making One Income Stretch: A Single-Parent Money Guide

One income with kids can make every ordinary thing feel loaded. The grocery top-up. The school email asking for $12 by Friday. The shoes that somehow fit last week and now look personally offensive.

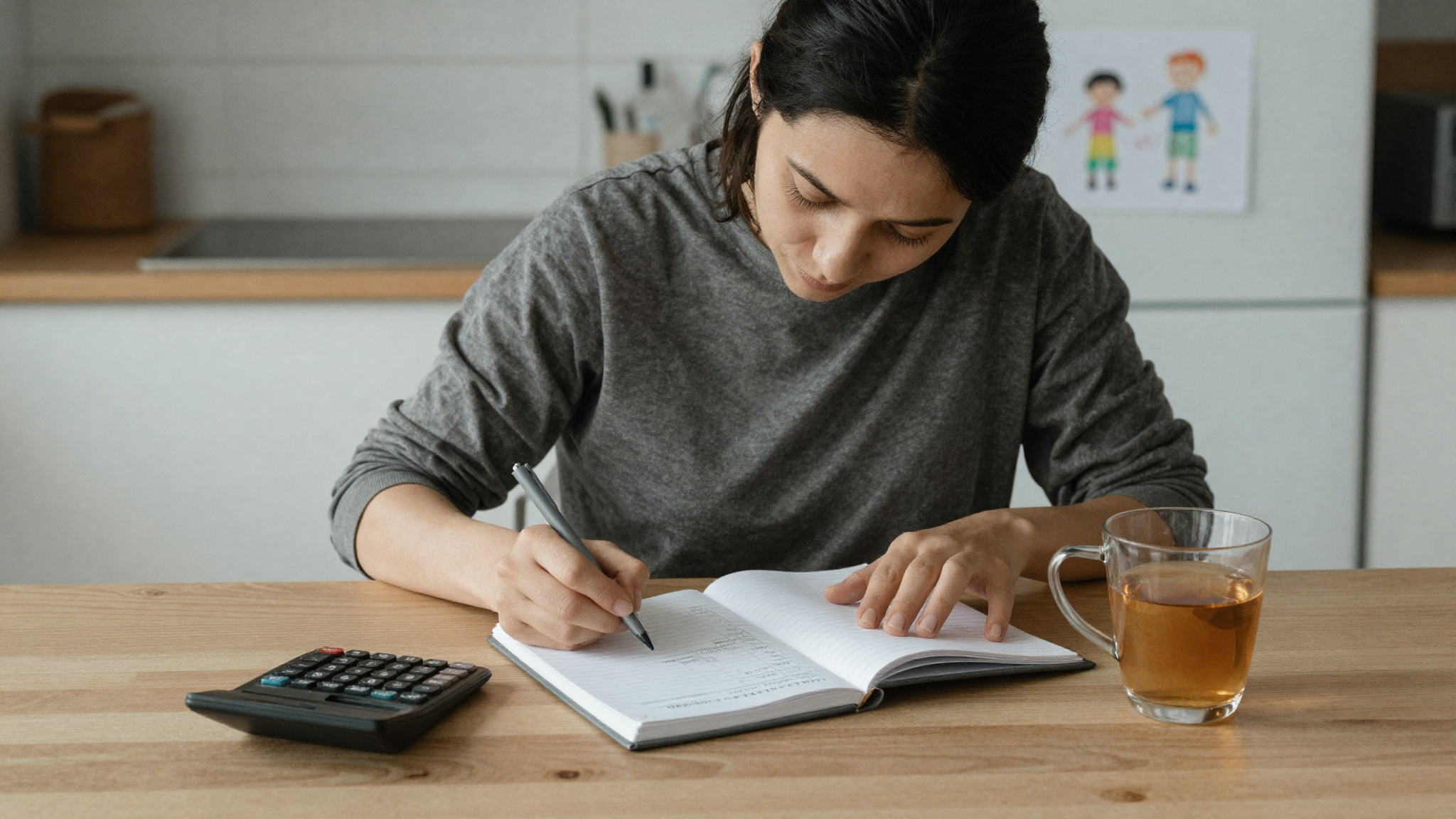

If money feels tight, it doesn’t mean you’re bad with it. Single-parent finances are often tight simply because one adult is doing the earning, planning, remembering, driving, feeding, soothing, and late-night adding up. A budget helps, but only if it survives real life.

This is the practical version: fewer pots, fewer lectures, more breathing room. The aim isn’t to become a spreadsheet person overnight. It’s to know what has to leave, what can bend, and where help may already exist.

Start with the money that has to leave first

Fancy budgeting systems tend to collapse the first week a child gets sick, the car makes a noise, or school announces a costume day with the confidence of people who don’t know your bank balance.

Use three pots instead: fixed bills, child basics, and everything else. Fixed bills are the roof-over-your-head money: rent or mortgage, utilities, insurance, phone, transport, debt payments. Child basics are food, school, childcare, medicine, clothes that actually fit. Everything else is the wobbly bit.

Automate what you can on payday, even if the amounts are small. When the non-negotiables leave first, you stop accidentally spending the rent in tiny, harmless-looking pieces. It’s deeply unglamorous, which is exactly why it works.

Claim everything you’re entitled to

This is where real money can hide. Not magic money, not free luxury money. The boring, form-filled kind that helps with food, childcare, health insurance, housing, utilities, school meals or income support.

If you’re in the U.S., USA.gov’s benefits page is a solid official place to start, because it points to food assistance, health insurance, housing help, utility help and state agencies. If you live elsewhere, use the official government calculator or benefits checker for your country, not a random blog promising hidden grants.

Child support or maintenance belongs in this conversation too. It can be emotionally messy, especially if co-parenting is tense, but money for a child isn’t a favour from one adult to another. It’s part of the child’s practical care.

Cut the costs that hurt least

Start with the money leaving quietly: subscriptions you forgot, delivery fees that became a habit, insurance that renewed itself with a tiny little smirk, apps the kids used once and abandoned.

Then look for swaps that don’t steal the good parts of life. Library books instead of buying every title. Second-hand uniform where nobody will notice. Batch-cooked pasta sauce for the night you know future-you will want takeaway. A snack shelf that saves you from emergency corner-shop prices.

Don’t cut the things that keep the house human first. The $4 coffee after a brutal appointment may be cheaper than the emotional crash it prevents. The trick is finding the leaks, not stripping every soft thing out of the week.

Watch the guilt tax

The guilt tax is the money you spend because one income makes you feel like your child is missing out. The toy after a hard goodbye. The bigger birthday than you can afford. The yes you give because separation already gave them enough no.

A small treat can be lovely. The problem is when guilt starts making the budget decisions and then leaves you alone with the overdraft later.

Kids remember a surprising amount that didn’t cost much: sofa dens, pancakes for dinner, being allowed to sleep in your bed after a sad day, someone showing up at the school thing. Presence isn’t a budget category, but it does a lot of heavy lifting.

Build the tiniest emergency buffer

A three-month emergency fund sounds lovely when you’re reading it from a life with spare money. In a one-income house, start smaller. $5. $10. The coins left after groceries. The refund you forgot was coming.

Name the pot something specific: school shoes, car noise, medicine, winter. A named pot is harder to raid because it already has a job, and it turns saving from a moral performance into a practical little shield.

The first goal isn’t wealth. It’s avoiding the next tiny crisis becoming a borrowing crisis. If you can build $50, that’s not nothing. If you can build $100, that can change a whole bad week.

When the sums genuinely don’t work

Sometimes the maths still doesn’t work. You cut the forgotten subscriptions, cook at home, claim the help, skip the extras, and the month is still too long. That isn’t a personal failure. That’s information.

If debt is growing, bills are late, or you’re choosing between food and heat, get support early. In the U.S., the National Foundation for Credit Counseling can connect you with nonprofit credit counsellors for budget and debt help. Outside the U.S., look for a regulated nonprofit debt-advice service in your country.

And if the money stress is part of the wider separation storm, keep the adult money panic away from the kids where you can. They need honesty in child-sized pieces, not the full weight of your bank app at midnight.

Frequently asked questions

Start with three pots: fixed bills, child basics and everything else. Pay or separate the fixed bills first, estimate the real child basics, then make decisions with what’s left. A simple budget you can keep using beats a detailed one that collapses by Thursday.

It depends where you live, but help can include food assistance, childcare help, health insurance, housing support, utility help, school meals and child support or maintenance. Use official government benefit tools first so you’re checking real eligibility, not guesswork.

If money is tight, start tiny: $5 or $10 when you can. The first goal is a small buffer for school shoes, medicine, car trouble or surprise school costs. Even $50 can stop one bad week turning into borrowed money.

That can happen, and it isn’t a character flaw. Check official support, child support or maintenance, and regulated nonprofit debt advice early. Be careful with companies that promise fast fixes or ask for money before properly reviewing your situation.

Leave the first comment

Share your thoughts

I'm for the parent doing it largely alone. I've done the single-dad decade - two homes, one income, the handovers, the very quiet Tuesdays - and I write from the far side of most of those days, with humour and hard-won calm. Not advice from above; a hand back from a few steps up the road.

More from DiegoWhat's getting you through right now? Be honest - we're all figuring it out.

No right answers here - tell us how it actually went. Someone reading needs to hear it.

Join the conversation